Research Report | MDA Space

Two-sats-a-day: The high-volume bet on global communications

All figures are as of Feb 6, 2026, in CAD.

Summary

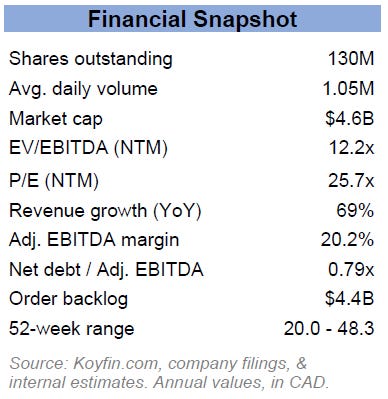

We recommend a Buy on MDA Space with a target price of $52.00, estimated at 15.0x 2027E EBITDA, representing 42% upside over 12 months. The Street is excessively discounting MDA due to the recent EchoStar contract cancellation and rumors of a SpaceX acquisition of Globalstar and maintains an overly conservative view on MDA’s transition from bespoke contracts to high-volume manufacturing. While consensus models anticipate EBITDA margin contraction and flat Satellite Systems revenue, we believe they underestimate the impact of AURORA rollout and a substantial pipeline of Canadian sovereign and commercial contracts. We expect the valuation gap to close through three primary catalysts:

Sovereign & commercial pipeline conversion represents $7B+ of Canada’s sovereign space spend, positioning MDA to potentially secure significant manufacturing deals as the nation’s leading space prime, and Telesat’s 100-satellite extension option provides significant future upside.

Execution milestones for the Montreal facility’s production ramp for Globalstar and Telesat will serve as validation of the AURORA platform’s profitability and manufacturing reliability.

U.S. dual listing: A prospective listing on the NYSE or NASDAQ would significantly expand liquidity and institutional access, and could trigger a re-rating, narrowing the current 75% valuation discount to US-listed peers.

Company Overview

Founded in 1969 as MacDonald, Dettwiler and Associates, MDA Space (TSX: MDA) is a Canadian aerospace contractor specialized in the design, manufacture, and operation of advanced space infrastructure. Brampton, ON is home to its headquarters and the Space Robotics Centre of Excellence, a 200,000 sq. ft. production facility and control center for in-orbit robotic operations, while the newly-expanded Montreal facility offers 185,000 sq. ft. to accomodate the AURORA satellite production line. Additional facilities and regional offices can be found in British Columbia, Nova Scotia, United Kingom, United States, and Isreal.

MDA is organized into three business segments:

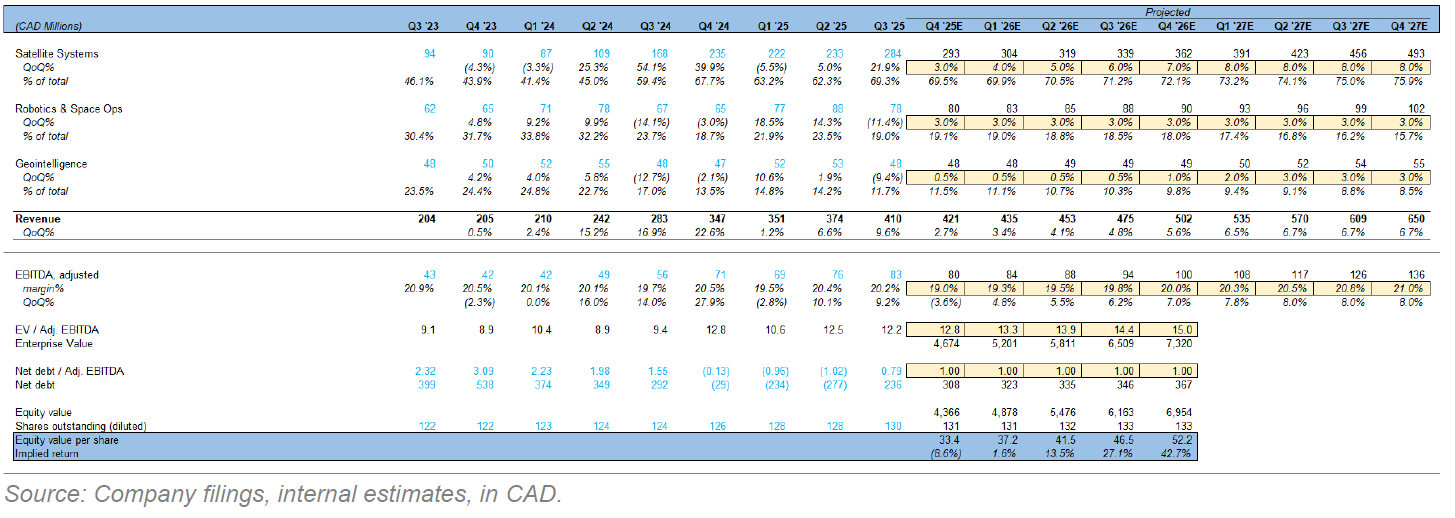

Satellite Systems - MDA’s largest revenue driver, it’s currently undergoing a paradigm shift from low-volume, customized builds to high-volume manufacturing, with production at the Montreal facility slated to ramp up to two satellites per day over the next eight quarters. At the center of this transition is the software-defined AURORA satellite. Unlike traditional analog satellites, whose functions and capabilities are fixed once launched, AURORA utilizes digital payloads that allow operators to recognfigure coverage and functionality dynamically while in orbit.

Robotics & Space Operations - a smaller but high-margin segment, at its core are the Canadarm3 and SKYMAKER programs. Unveiled in 2024, SKYMAKER is a suite of modular space robotics hardware and software, alleviating the need to design and manufacture custom systems that can’t be reused. Canadarm3 is a $1B contract to deliver an autonomous system for NASA’a Lunar Gateway program, a planned lunar orbit space station.

Geointelligence - MDA’s Data-as-a-Service arm directly operates satellite constellations, selling satellite imagery and analytics for climate, defense, and maritime monitoring. The upcoming 2026 launch of its CHORUS constellation will provide high-resolution, near-real-time observation of global mid-latitude regions.

MDA is well-established within the Canadian ecosystem, and a primary beneficiary of sovereign space infrastructure spending. Beyond its domestic stronghold, MDA is solidifying its position as a prime contractor within the US defense and commercial ecosystems. In January 2026, the company was approved as a contractor for the US Missile Defense Agency’s SHIELD program. By leveraging its status under agreements such as the National Technology Industrial Base (NTIB) and United-States-Mexico-Canada Agreement (USMCA), MDA functionally competes as a ‘domestic’ player for lucrative defense contracts.

Investment Thesis

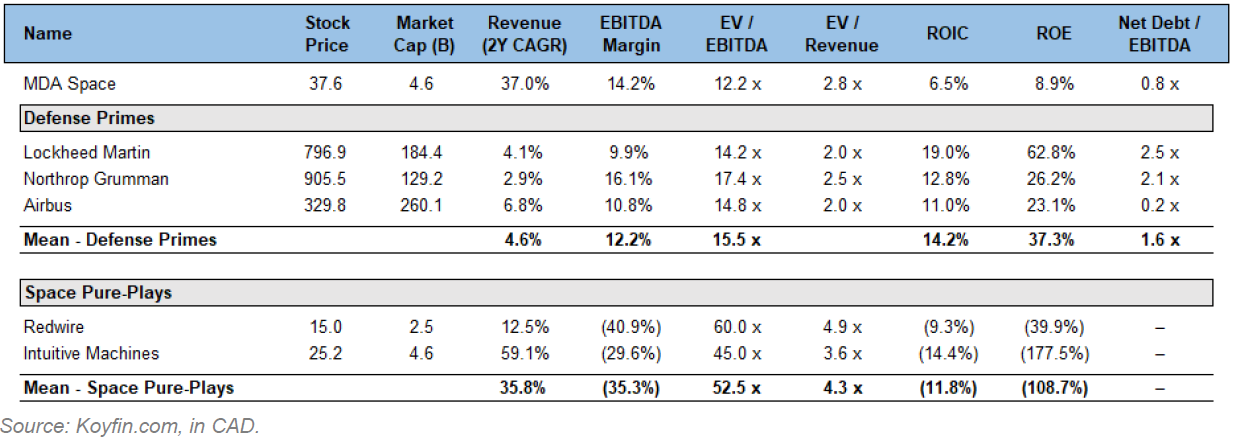

MDA trades at a significant discount to US peers on a 2027E EBITDA basis, highlighted by the York Space Systems (YSS) IPO seeking a $4.25B valuation. While YSS reports negative EBITDA, we derive a synthetic 43x EV/EBITDA multiple by applying MDA’s 20% margins to YSS’s $512M TTM revenue. This shows a significant valuation disconnect, as MDA has triple the revenue, 20% EBITDA margins, and 5.1x the backlog, yet trades at 12.2x EBITDA. While a ‘Canada discount’ may persist due to preferences for domestic manufacturing, we believe the current gap is unsustainable.

MDA is transitioning to volume manufacturing from bespoke engineering projects with its 185,000 sq. ft. Montreal facility, designed to produce two satellites per day. While we anticipate near-term margin pressure as production ramps, the shift to standardized assembly-line production should drive EBITDA margins towards 21% through operating leverage and superior product quality.

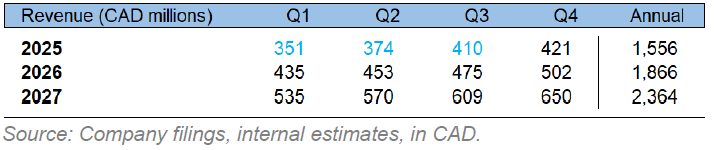

MDA’s robust $4.4B backlog represents ~2.4x coverage of 2026E sales, acting as a multi-year engine for cash flow conversion. This visibility allows MDA to ramp production while funding operations through internal cash flows. The milestone-based structure of these contracts provides liquidity throughout the manufacturing cycle,

As Canada’s preferred domestic prime contractor for space infrastructure, MDA is the primary beneficiary of a $6B+ multi-decade spending cycle focused on Arctic security and earth observation. Programs like RADARSAT ($1B) and ESCP-P ($6.8B+) are classified as ‘mandatory replenishment’ missions, requiring the government to replace aging satellite fleets to maintain uninterrupted surveillance and monitoring. This creates a recession-resistant revenue floor, as the contracts are based on critical service continuity rather than discretionary spending, and acts as a counterweight to the cyclical spending of commercial firms.

Space is now a core national security domain as global gov’t space spending reached $137B in 2025, with a record 54% allocated to defense. This shift is fueled by a broader rearmament cycle, as Canada has accelerated its timeline to hit the NATO spending target of 2.0% of GDP by March 2026 (vs. 1.37% current), while America’s defense budget is projected to cross $1T in 2025 (3.5% of GDP). While MDA is a Canadian firm, it’s tightly integrated into the US market through various frameworks: USMCA shields MDA from tariffs, while NTIB allows US defense agencies to treat Canadian entities as ‘domestic’ for procurement purposes. In January 2026, MDA was approved as a contractor for the US Missile Defense Agency’s SHIELD program ($151B total funding), cementing MDA’s position as a critical multinational player.

SatixFy acquisition brings digital payload design in-house, which we believe will reduce supply chain risk and expand margins. By owning the IP for its radiation-hardened chipsets, MDA can now seamlessly design and modify these integral components and avoid the heavy markups of external vendors. Additionally, a strategic partnership was inked with Maritime Launch Services in Q3 ’25 to develop domestic launch capabilities. This collaboration strengthens the domestic ‘ground-to-orbit’ pipeline and gives MDA influence over launch integration.

MDA exhibits superior capital flexibility with an adjusted net debt/EBITDA of 0.79x, having successfully funded its infrastructure expansion through internal cash flow and customer prepayments. This disciplined approach positions MDA for a significant free cash flow inflection in late 2026 as capex declines from its peak of $250M, eventually to a maintenance level of $30-$40M. As a consequence, MDA enters its execution phase with the ability to fund accretive M&A or capital returns from a position of strength while peers remain capital-constrained.

Risks

Customer concentration and contract slippage: Contracts with Telesat ($2.1B) and Globalstar ($1.1B) now represent 73% of MDA’s $4.4B backlog, tethering performance to the deployment schedules and financial health of just two firms. While these provide high revenue visibility, they also introduce significant risk, as any financing hurdles or deployment delays from either customer would impair MDA’s revenue recognition and margins.

Execution risk in scaling manufacturing: MDA recently finished its Montreal facility expansion, intended for volume manufacturing of its AURORA line. While it’s designed for a peak capacity of two satellites per day, 2026 will be a test period of a few dozen units. Production is forecasted to accelerate in 2027, as Telesat is aiming to have at least 156 satellites in orbit by the end of the year. Any persistent internal bottlenecks or quality failures would not only defer high-margin revenue but could also trigger liquidated damages or force MDA to incur additional debt, degrading their balance sheet strength.

Market share erosion from SpaceX and defense primes: While we believe MDA is solidly entrenched as the supplier for Canadian government projects, its commercial positioning is threatened by incumbents such as Lockheed Martin (LM 400), Northrop Grumman (ESPAStar), and SpaceX (Starshield) with deep pockets and operationalized high-volume satellite lines. The loss of the $1.8B EchoStar contract – following EchoStar’s $17B sale of its spectrum licenses to SpaceX – demonstrates that vertically-integrated giants can buy out MDA’s customer base to support their own satellite fleets, even if MDA’s contract protections (full cost-plus-fee recovery) buffer against direct financial loss.

Valuation

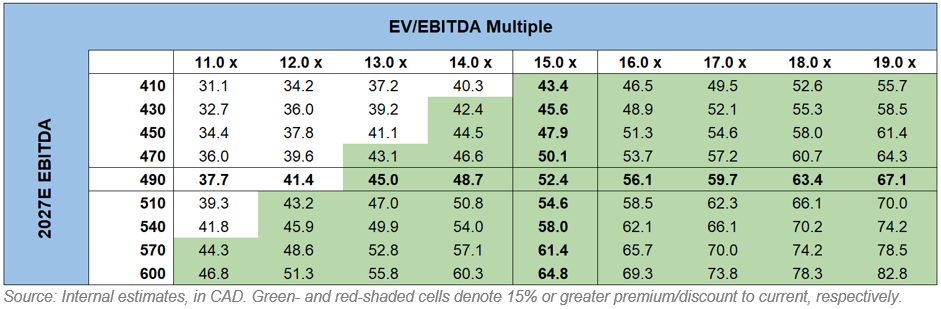

We value MDA at 15.0x 2027E EBITDA, implying a fair value of $52.00 per share, while the firm trades at 12.2x, a discount to the Defense Prime average of 15.5x despite significantly higher growth. While we anchor our target to Defense Primes, we note that pure-play peers trade a staggering 50x. This includes our synthetic multiple from YSS. Thus, we believe applying a 15.0x multiple is a conservative and justified approach that reflects MDA’s operational maturity and sovereign entrenchment.

Each 1.0x turn in EV/EBITDA moves fair value by $3.50. In the bear case, MDA faces internal and client-side delays, while anticipated sovereign and commercial backlog additions fail to materialize. In this scenario we model a contraction to 10.0x, implying $34.00 per share. In the bull case, manufacturing volumes ramp smoothly and MDA wins high-margin US defense contracts via SHIELD. In this scenario we re-rate to 18.0x and derive a fair value of $63.00 per share.

In our bull and bear cases, we varied only the EV/EBITDA multiple for an estimate of changes in share price for simplicity. We recognize the limitations of not modelling growth rates and backlog additions for each case, but thought a rough estimation of our price target range would be nonetheless insightful.

Relative Valuation Summary

Summary Financials & Projections

Target Price Sensitivity Analysis

Disclaimer

At the time of publication, the author holds a long position in MDA.

The information provided in this post is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Readers should conduct their own research or consult a financial professional before making investment decisions. Investing involves risks, including the potential loss of capital.