Research Report | Kneat

Regulatory tailwinds fuel strong ARR growth in an underexplored niche

All figures are as of July 16, 2025, in CAD.

Summary

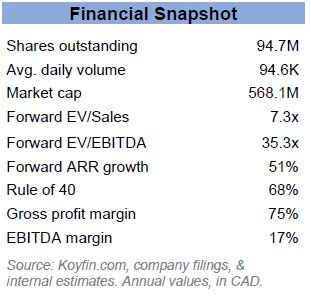

We recommend a Buy on Kneat with a target price of $8.00, estimated at 6.5x 2026E revenue, implying 36% upside over 12 months. Our core thesis is that Kneat is at an EBITDA inflection point while simultaneously expanding its TAM, setting up a transition toward profitability-driven valuation. Kneat’s digital validation (eVal) platform is emerging as the industry standard in life sciences, supported by a land-and-expand strategy and deep enterprise adoption. With annual recurring revenue (ARR) of $63.5M (68% 3Y CAGR), 75% gross margin, and EBITDA turning positive, Kneat is a Rule of 70 company that has reached the scale where operating leverage is materializing. Regulatory tailwinds and an expanding partner ecosystem support continued >50% ARR growth as Kneat broadens its TAM from $2B to $7B across adjacent regulated verticals. Kneat is continuously enhancing its platform, adding new modules and use cases to deepen adoption and extend its moat. Our 6.5x 2026E sales valuation, a modest premium to peers, reflects Kneat’s superior growth, margins, and visibility.

Investment Thesis

Category leadership in eVal: Kneat is cementing its leadership position, displacing legacy paper systems across the life sciences industry. 8 of the 10 largest global pharma companies already use the Kneat Gx platform. With virtually zero churn and 151% net revenue retention (NRR), we see evidence of high switching costs and durable recurring revenue visibility. Increasing regulatory complexity further reinforces Kneat’s position and widens its moat as more firms adopt digital solutions.

Land and expand growth engine: Kneat’s growth is shifting to a balanced engine of new logo wins and recurring expansion. It has been averaging five new logos per quarter, a pace we project will nearly double as Kneat moves to focus on mid-market firms and leverages its partner network. Partnerships with Körber, ALTEN, and Capgemini extend Kneat’s reach into new verticals and broaden its TAM. As customer concentration declines and annual contract values (ACV) rise, we expect new logo growth to become a key driver of ARR growth through 2026.

Improving profitability and cash generation: With a 75% gross margin, 17% EBITDA margin, and a 68% Rule of 40 score, we predict Kneat’s unit economics to continue to strengthen as it scales. Payback periods are expected to shorten, while free cash flow has recently turned positive, signaling growing operating leverage. These trends enhance Kneat’s ability to fund expansion internally while maintaining flexibility to access external capital as opportunities arise.

Company Overview

Healthcare – Health Information Services

Kneat.com Inc (Kneat) is a Canadian software-as-a-service (SaaS) firm that provides eVal software for regulated industries, primarily the life sciences (biotech, pharma, medical devices). Its flagship product, the Kneat Gx platform, is a customizable, off-the-shelf digital alternative to legacy paper-based systems that improves accuracy, compliance, and efficiency. Kneat operates on a subscription model with supporting implementation and training services.

Business Analysis

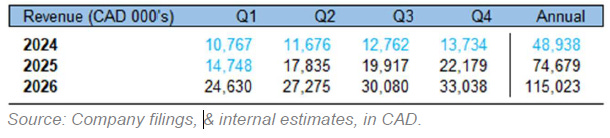

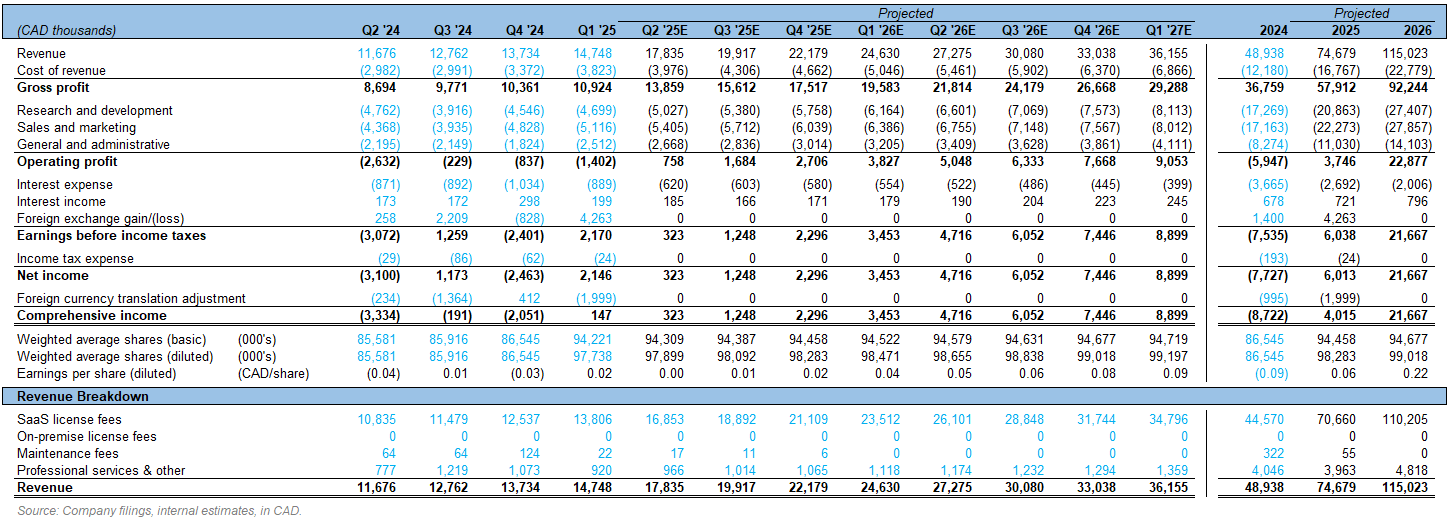

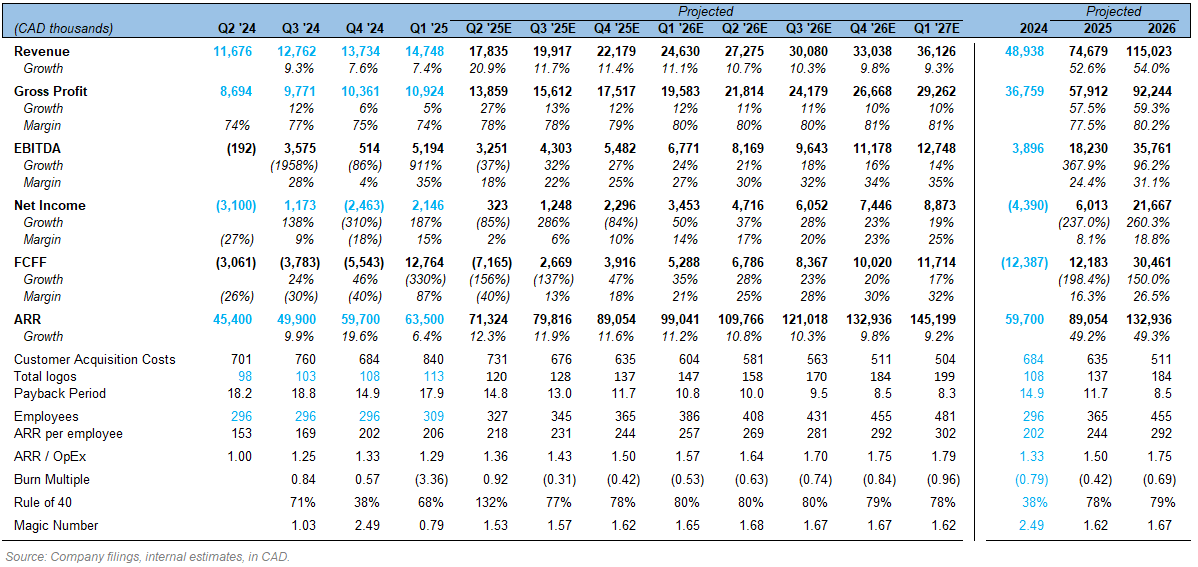

Kneat has grown ARR at a 3-year CAGR of 68%, hitting $63.5M in Q1 ’25. A large portion has been due to upsell to existing customers, with Kneat boasting an impressive 151% net retention rate (NRR), up from 138% in ’23. This is unsustainable in the long term, but we see plenty of room for upsell remaining, supported by Kneat’s strong R&D spend and focus on broadening Kneat Gx’s functionality. We project NRR to decrease slightly to 138% by Q2 ’26, at which point 77% of new ARR will be due to upsell (from 87% Q1 ’25) and 23% from new logos (from 13% Q1 ’25). Overall, we believe ARR will grow 51% CAGR over the forecasted period.

Kneat’s gross margin is 75%, in line with expectations for a SaaS firm, and we project this growing to 80% by Q2 ‘26 as Kneat expands and benefits from economies of scale. EBITDA flipped positive in ’24, and FCFF, while still volatile, flipped in Q1 ’25. We have seen positive EPS in recent quarters, and believe this trend will continue, reaching $0.05 in Q2 ’26.

Revenue concentration has declined to 50% among Kneat’s ten biggest customers (from 67% in ’21) and as of Q1 ’25 no single customer is more than 10% of revenue. Kneat has been winning about five logos a quarter at an average customer acquisition cost (CAC) of $750K over the last 4 quarters. As Kneat turns to marketing to mid-market firms, we anticipate acceleration in new logo wins to 9 per quarter and declines in top ten customer concentration (to 43%) and CAC (to $580k), which will boost operating margins and facilitate multiple expansion.

We estimate Kneat’s annual contract value (ACV) for new logos to be $150K - 200K, and modelled Q2 ’25 at $150K to represent Kneat’s focus on mid-market firms. However, due to Kneat’s position as a leader in Validation and continued investment in its platform, it will benefit from strong pricing power and we believe ACV will rise to $220K by Q2 ’26. We also foresee a step-up in ACV in H2 ’25 as this is likely when Kneat will roll out its AI-integrated platform, representing a boost in functionality and productivity for customers. High CAC and low starting ACV mean Kneat’s contracts have fairly long payback periods (18 months in ’24). We should see this decline to 10 months by Q2 ’26 as Kneat scales its operations, reducing the perceived riskiness of its business and driving multiple expansion.

Kneat is investing significant capital in R&D to extend its software beyond its validation niche into related workflows such as Commissioning & Qualification, tech-transfer, batch-record management, and drawing management. At the same time, it’s laying the groundwork to evolve the platform into a comprehensive Quality Management System (QMS). In the near term, Kneat is expanding into life science-adjacent industries, such as manufacturing, and other highly regulated industries like F&B, exemplified by a 3-year deal inked with a multinational F&B producer in Q1 ’25. With $74M in total cash, including $22M in financing maturing Q1 ’28, Kneat can fund this roadmap without additional dilution or refinancing risk.

Industry Analysis & Competitive Positioning

Kneat’s current TAM, composed of core life science firms, is $2B, and independent forecasts of growth range from 10-13% CAGR over the next 5 years. Expansion into life science adjacencies and food & beverage will bring TAM to ~$7B. In the mid- to long-term, Kneat has stated it plans to target other highly-regulated industries such as aerospace & defense.

Kneat’s ‘State of Validation 2024’ report estimates 30% of life science firms have already implemented eVal, while 53% have plans to do so. Sentiment in the life sciences is cautiously optimistic, and we are seeing orders in bioprocessing consumables (e.g., filters, resins) rebounding for firms like Thermo Fisher, a Kneat customer. This suggests capex and IT budget bumps will follow soon after and fuel Kneat’s ARR growth. The FDA’s upcoming finalization of Computer Software Assurance (CSA; expected late ’25) and the EU’s GMP Annex 11 revision (expected mid ’26) are additional tailwinds for eVal, as both frameworks tighten data integrity expectations and explicitly promote implementation of automated digital solutions.

Kneat is already well established as a reputable provider of eVal among top life sciences firms and benefits from customers’ high switching costs, boasting virtually no churn. Once Kneat lands a customer, switching to another platform is highly unlikely given the regulatory risk of re-validating all workflows, migrating data and retraining staff. A handful of private vendors (e.g., ValGenesis, MasterControl, Tricentis, and Sware) also offer eVal, but either package it within a broader QMS or are much smaller pure-plays with limited reach. We expect Kneat to face competition from these players in the mid-market segment, but competitors lack the ability to penetrate the large-cap segment. Mega-cap names such as Veeva and IQVIA also offer eVal, though it contributes <5% of revenue. IQVIA’s focus remains on its Customer Relationship Management (CRM) platforms rather than expanding into eVal. Veeva, which has historically operated through Salesforce, plans to migrate to its own platform in Q3 ’25, while IQVIA recently announced a partnership with Salesforce for its life sciences CRM. We believe this new dynamic will be the main focus for both firms, making a pivot into eVal unlikely in the next 2-3 years.

Kneat’s channel partner strategy is an important part of its growth, expanding its global reach and service capabilities. Partners can integrate Kneat Gx with their own products or sell Kneat Gx standalone, and are responsible for implementation and maintenance. Kneat’s focus on expanding this program will meaningfully boost ARR growth by accelerating brand recognition without a proportionate headcount increase. We see this as a scalable route to penetrate new verticals without proportionate head count increases, counteracting some of the program’s margin dilution.

Risks

Our valuation assumes Kneat not only deepens penetration in core life sciences beyond the largest names, but also lands adjacent suppliers and builds F&B-specific expertise to win new logos. These moves will require tiered pricing and lighter-touch implementation for mid-market life science firms, and additional certifications (e.g., ISO 22000) and compliance requirements (e.g., HACCP, FSMA) for F&B. While some of Kneat’s reputation and brand will be recognized by the new vertical, firms may be hesitant to adopt Kneat’s platform until it has demonstrated competency in their processes and regulations. Kneat has a healthy net cash position of $44M, but delays in expansion plans could see these reserves deplete, and force additional equity or debt raises.

While Kneat is a market leader in eVal, it could still lose market share to competitors if they price more aggressively or leverage larger service and partner networks. A few in particular have deeper pockets and could challenge Kneat’s position, such as Veeva ($46B), IQVIA ($29B), Tricentis ($1.5B), or MasterControl ($1.3B). However, these platforms cover a broad range of functions, and we believe Kneat’s eVal focus and expertise make them the more attractive option for many firms.

If sector headwinds persist, we could see delays in IT budget and capex expansion. Delays in regulatory updates could push back eVal adoption, and any regulatory failures involving Kneat’s platform would be damaging to its reputation and push potential customers towards rivals. We view these risks as low probability but potentially material to Kneat’s growth and valuation.

Valuation

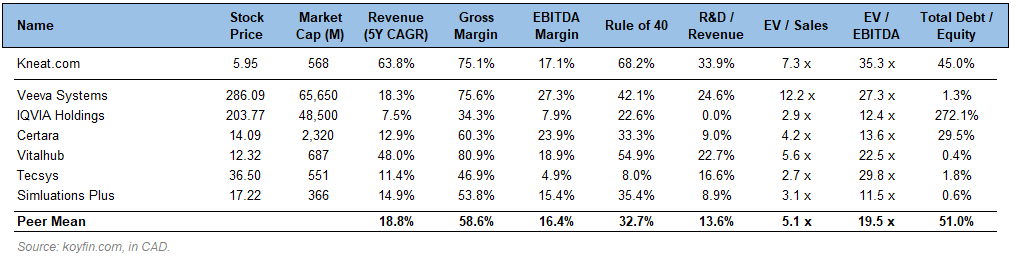

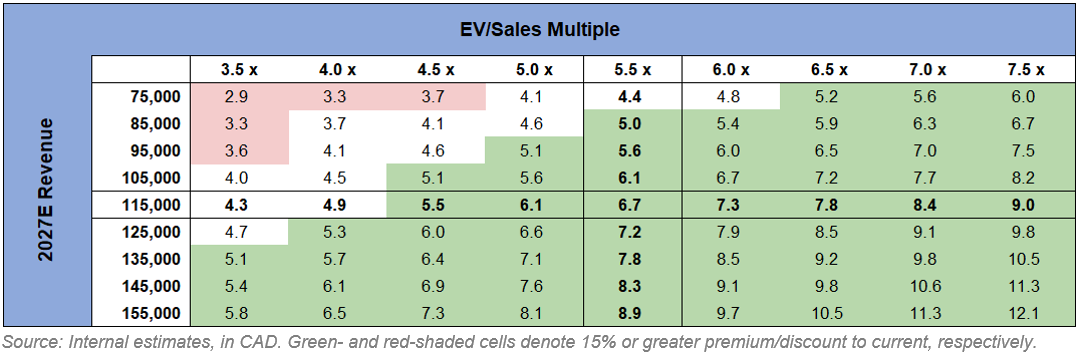

With our model projecting a 3Y ARR CAGR of 51% through 2026, we value Kneat at 6.5x 2026E sales, implying an enterprise value of $820M. This is a premium to the peer average of 5.1x EV/Sales, justified by Kneat’s best-in-class growth, strong margins, low churn, and leadership position within a heavily regulated niche. After adjusting for net debt, we arrive at our price target of $8.00 per share, 36% above current.

Sector multiples have been compressed in recent periods due to high interest rates, macro uncertainty, and muted end-market demand. As demand normalizes, we should see this compression reverse. Additionally, as Kneat turns profitable, wins logos in new verticals, and regulatory changes crystallize, we believe further re-rating is possible.

Each 1.0x turn in EV/Sales moves fair value by $0.86. In the bear case, customer budgets tighten further and Kneat struggles to penetrate new verticals and mid-market life science firms. In this scenario we model a contraction to 3.0x and believe the stock would drift to $4.00. In the bull case, Kneat grows faster than anticipated, landing large enterprise contracts in adjacent regulated industries and expanding its footprint within existing life sciences customers. Accelerated rollout of AI-integrated functionality would further boost adoption and margins, supporting a re-rating to 8.5x, or $10.50 per share. Overall, we view Kneat as a high-quality growth compounder trading near trough multiples, with a long runway for re-rating as profitability and adoption scale.

Relative Valuation Summary

Kneat’s most direct competitors are largely private firms such as ValGenesis, MasterControl, and Sware, so we built the peer set by choosing enterprise B2B SaaS firms selling into healthcare and life sciences.

Summary Financials & Projections

Target Price Sensitivity Table

Disclaimer

At the time of publication, the author holds no position in KSI.

The information provided in this post is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Readers should conduct their own research or consult a financial professional before making investment decisions. Investing involves risks, including the potential loss of capital.